‘‘We are attentive to the risks of potential further upward pressure on inflation and inflation expectations. The Committee is determined to take the measures necessary to restore price stability. The American economy is very strong and well positioned to handle tighter monetary policy.’’

Jerome Powell, March 2022 FOMC press conference

I am not sure everybody has grasped yet how important was the message Jerome Powell sent yesterday during the FOMC press conference. While market commentators are focusing mostly on the mere 25 bps hike and the lack of details on Quantitative Tightening, I believe they are missing the point: the forward guidance was very hawkish, and very clearly so.

This piece will try to unpack the Fed decision for you, and more specifically:

- Go through the most important, and yet overlooked parts of Powell’s strong forward guidance for what the Federal Reserve reaction function will look like in the near future;

- How bond markets and risk assets reacted, and how I believe investors should consider adjusting their portfolio accordingly.

Without further ado, let’s jump right in!

Hawkish to the Power of Four

Actually, before we jump right in. If you are interested in any kind of partnership, sponsorship, or in bespoke consulting services feel free to reach out at TheMacroCompass@gmail.com. Back to it: Powell is becoming more and more hawkish as time goes by. I identified 4 key hawkish messages he conveyed yesterday, let’s go through them.

1. Wage growth is very strong, the labor market is extremely tight, households’ balance sheet are healthy: this is the strongest economy in a while.

Powell started the press conference by telling us how strong is the US economy. He deliberately chose to focus on the positive aspects of the labor market, and explicitly ignored any (evident) signposts that could counter his very bullish macro assessment. For instance, he referred multiple times to a very tight labor market which is causing wage pressures left, right and center: true in nominal terms, but we all know real wages have been shrinking for more than one year. Powell didn’t mention that. Most importantly, he often referred to a supply/demand imbalance in the labor market: tons of job openings, not enough workers. ‘‘The labor market is hot.’’ Sure, but the constrained supply of workers also acts as a big drag for potential long-run real GDP growth: a lower labor force participation rate (blue, left hand side) constraints the supply of available labor, which is negative for potential economic growth and drags down the equilibrium real interest rate (orange, right hand side) at which the economy can function. This part was also largely ignored.

Source: The Macro Compass elaboration of Bloomberg data

By focusing only on the positives, Powell tried to prepare investors for the (enhanced) hawkish forward guidance.

2. The Fed is very confident (!) that the private sector can not only withstand, but flourish (!!!) in the face of less accommodative monetary policy

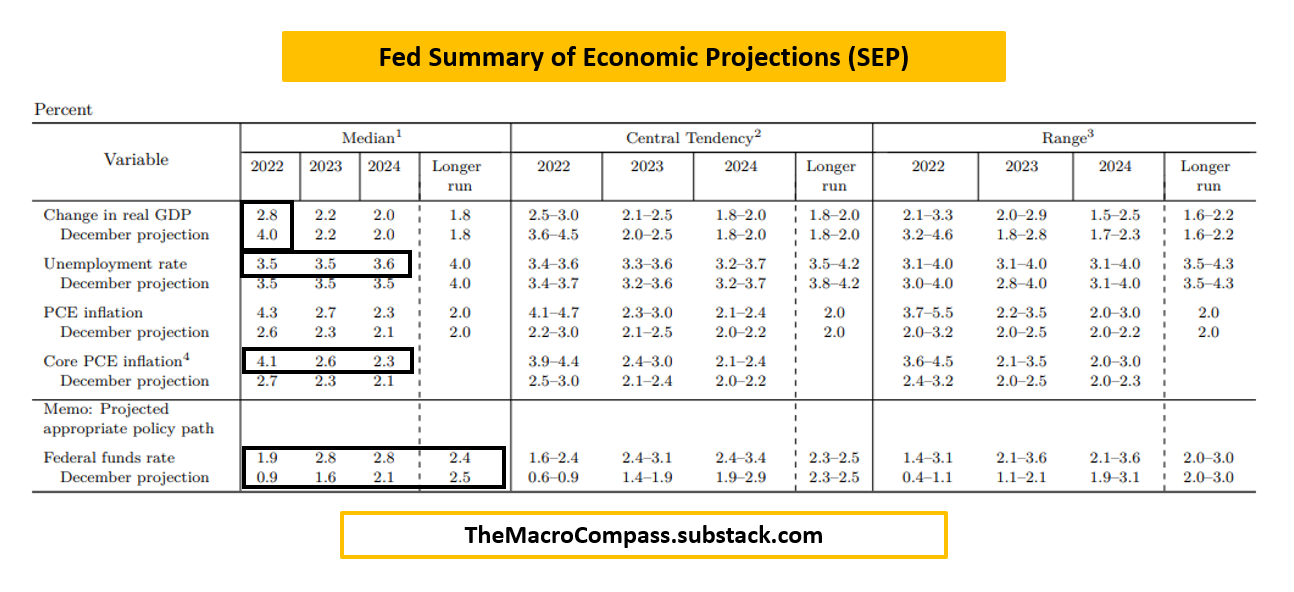

Really, this is quite a statement. It goes to show how confident is the FOMC about the strength of the economic cycle in the US, and therefore how aggressive they can be in tightening monetary policy without impairing the economic recovery at all. This was also reflected in the Summary of Economic Projections (SEP):

Source: Federal Reserve website

Notice how:

- Federal Funds rate are now assumed to be 1.9% by December 2022, but most importantly at 2.8% in 2023 - which is 40 bps above the longer run neutral Fed Fund rate;

- Even with this sharp tightening of monetary policy to above-neutral levels, real GDP growth is expected to be comfortably above trend and unemployment rate to stay at 3.5% for the next 3 years;

- And that even with this sort of tightening, core inflation forecasts are still above the symmetric 2% Fed target.

Effectively, the Fed thinks the cycle is so strong that it can easily withstand a relatively sharp tightening back to neutral rates, and even ‘‘flourish’’ with interest rates above neutral levels: a truly impressive assessment!

3. The FOMC is attentive to the risks of potential further upward pressure on inflation and inflation expectations. The Committee is determined to take the measures necessary to restore price stability.

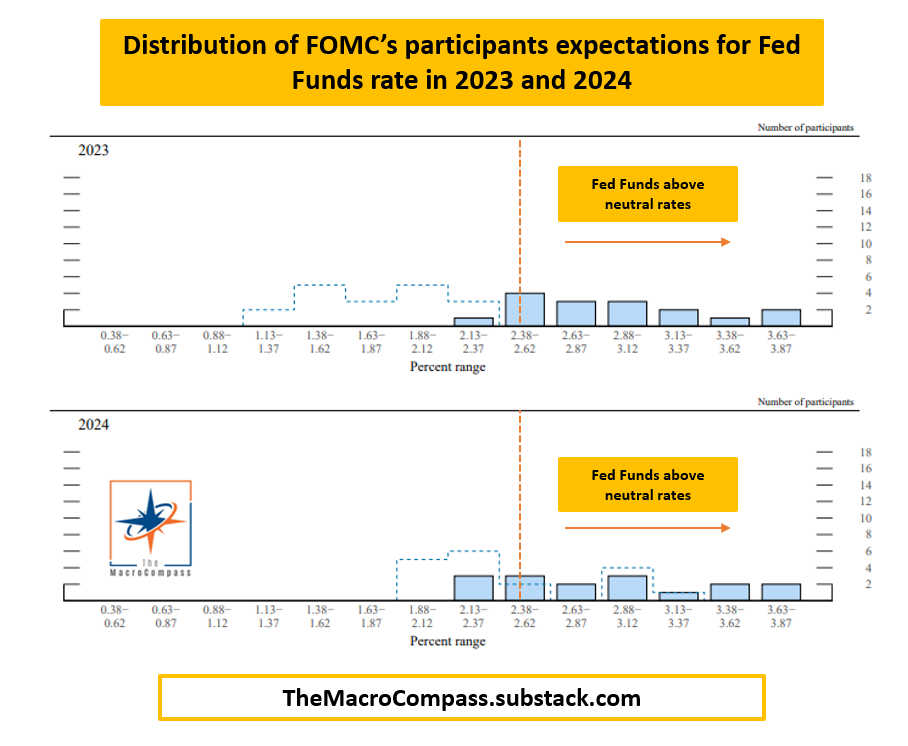

In this piece I published 10 days ago, I explained how the probability distribution of US inflation expectations over the next 5 years had not only shifted to a higher average level (>3% for PCE, the inflation indicator tracked by the Fed), but its right tail had dangerously become fatter: traders now price in a non-negligible probability of very high inflationary prints between 2022 and 2027. That’s a scary proposition for Powell, which wants to make sure inflation expectations remain anchored around 2% and expectations for high inflation do not become anchored in investors’ mind. How do you that? You explicitly tighten monetary policy above neutral rates.

Source: Federal Reserve website

The chart above shows the distribution of FOMC’s participants expectations for the appropriate level of Fed Funds rate in 2023 and 2024; notice that their own median estimate for neutral rates is around 2.4%. The large majority of FOMC members wants to see Fed Funds rate well above 2.4% in 2023 and 2024, with 7 or 8 Committee members projecting Fed Funds rates at or above 3% by then. Explicitly tight. Which brings me to the fourth important point.

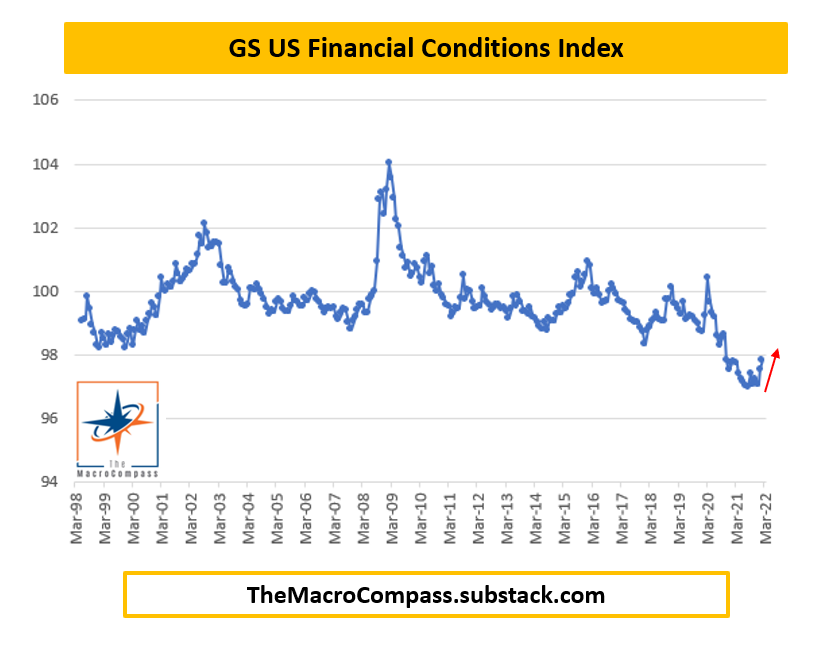

4. Financial conditions are one of the key transmission mechanism for monetary policy, and we will have to see tighter financial conditions to achieve our price stability targets.

Financial conditions reflect the degree of tightness the private sector faces when trying to secure new sources of financing. In December 2021, Powell was asked multiple times about financial conditions tightening and he said he wasn’t impressed by the pace of such move. This time, he went one important step further: he said financial conditions must tighten in order to help the Fed achieve its objectives (after all, he believes the private sector can easily handle this, right?). The key components of any respectable financial conditions index are: (real) yields, corporate bond spreads, mortgage rates, equity valuations and FX levels.

Source: Bloomberg

If you think the sell-off in equities, move up in USD and mortgage rates, and the widening in credit spreads we have seen this year is impressive…the chart above will serve as historical context for you to think again. What was that good old saying again? ‘‘Don’t fight the Fed’’.

Market reaction and portfolio ideas

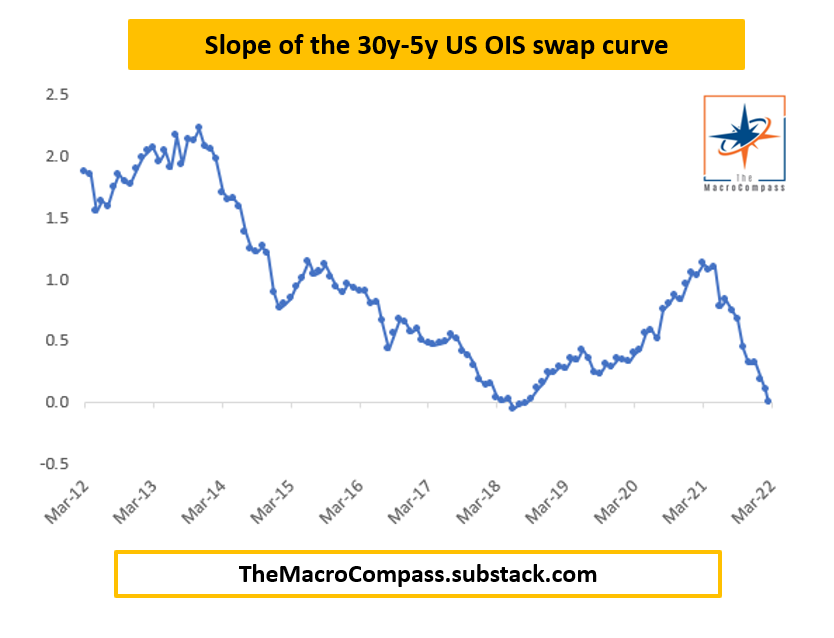

As the Fed promised to convincingly tighten monetary policy and market participants understand the impulse of growth is fading away (contrary to the super rosy assessment Powell is making) at the same time, yield curves continued their relentless flattening and inverted across important tenors. Here is an update for my preferred ‘‘inversion’’ metric (more on it in this piece):

Source: The Macro Compass elaboration of Bloomberg data

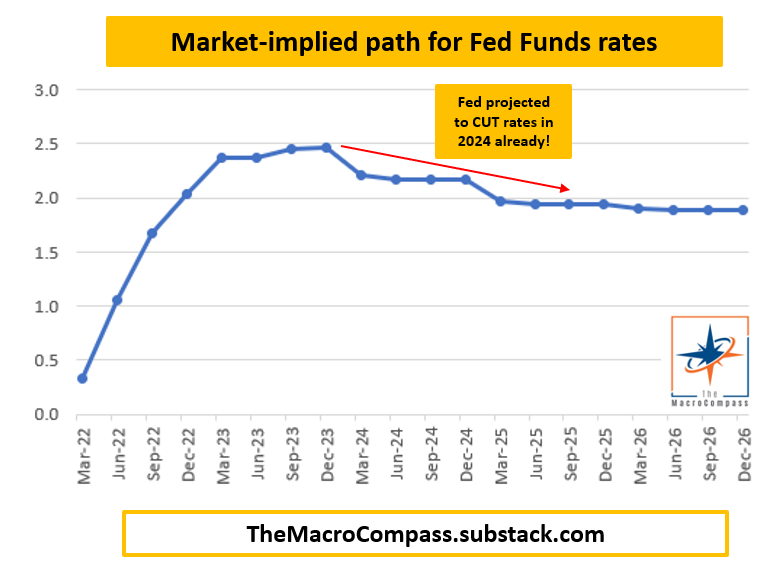

The slope of the 5y-30y US OIS curve became negative again following yesterday’s FOMC statements, and it’s now trading consistently around zero for weeks. Also, Fed Funds future project 30 bps cuts (!) from Powell in 2024. Yes, you read correctly: cuts.

Source: The Macro Compass elaboration of Bloomberg data

On the other hand and to my surprise, credit spreads and equities performed very well post FOMC conference: perhaps the lack of details over Quantitative Tightening and the removal of the biggest tail risk (50 bps hike) helped, but I believe the biggest reason behind the rally was a good old short positioning squeeze.